The Tokenized Money Stack

Four Powers, One Architecture, Zero Agreement

Money presents itself as uniform. A unit of cash, a bank deposit, and a reserve balance at the central bank are treated as equivalent units of account and means of payment. They circulate at par and move across balance sheets without friction in normal conditions.

But this equivalence does not arise on its own. It rests on institutional arrangements that align distinct liabilities within a single monetary system.

What is known as singleness of money, the principle that all forms of a currency trade at par with one another, depends on a framework of rules, public backstops, and institutional credibility. A commercial bank deposit and a central bank reserve differ in counterparty risk, liquidity, and regulatory treatment. Yet they still trade at par because deposit insurance protects depositors, central banks provide lender of last resort support, and capital and liquidity requirements constrain bank balance sheets. This structure has long underpinned monetary stability, even if it rarely attracts attention outside periods of stress.

The reason it matters now is that this hidden architecture is being rebuilt in public. Right now, without a single headline capturing the full picture, the plumbing of the global economy is being replaced by a new stack—which we decided to call the tokenized money stack. Four major powers—America, China, the United Kingdom, and the European Union—are each racing to build the future of money. And each, when you look closely, is building something subtly but critically different.

Most analysts frame this as a competition: dollar stablecoins versus the digital yuan versus tokenised deposits versus retail CBDCs. What those see is a monetary cold war, fought in code. But that framing misses something important. Each power is building a different piece of the same architecture—the layer it was historically equipped to build —while remaining functionally blind to the layers it most urgently needs.

History explains how each power got here. It also explains why each one is stuck.

The Architecture

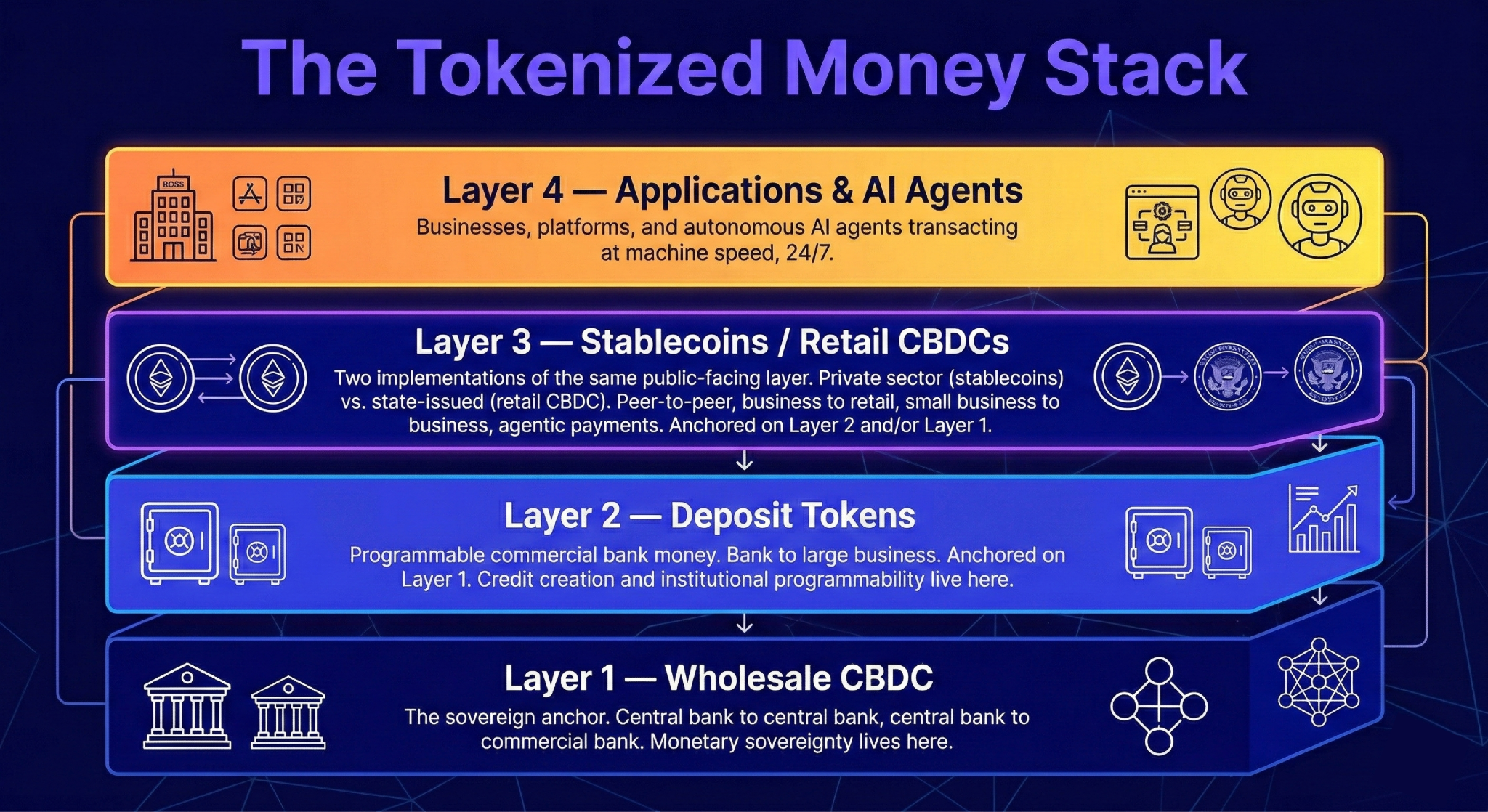

Before mapping what each power is building, it helps to be precise about what a complete tokenized money stack—which only exists in theory at this point—actually requires.

At the base sits the wholesale CBDC—the sovereign anchor. This is where monetary sovereignty lives. It enables central bank to central bank settlement, and central bank to commercial bank connection. Nothing above it is truly sovereign without it.

Above that sit deposit tokens—commercial bank money issued onto a blockchain by regulated banks, anchored on the wholesale CBDC beneath. These differ from tokenised deposits, which are an interbank settlement tool that stays within the banking system and never reaches clients directly. Deposit tokens do: a bank client can instruct their bank to mint tokens against their deposit and hold them on a public chain.

At the public-facing layer sit stablecoins and retail CBDCs. This is where a critical distinction is often missed. Both of those things (stablecoins and retail CBDCs) could serve the same use cases: peer-to-peer payments, business to retail, small business to business, and increasingly agentic payments between AI systems operating autonomously. A retail CBDC is the state’s version of this layer; a stablecoin is the private sector’s. The function could be the same. The difference lies in the governance.

Finally, above everything sits the application layer—businesses, platforms, and AI agents—where the value of programmable money is ultimately realised.

We do not yet know which of these layers will prove most valuable. But history offers a guide. The late Clayton Christensen called it the “law of conservation of attractive profits”: when a layer becomes modular and commoditized, attractive profits migrate to an adjacent layer. As Tim O’Reilly observed in his landmark Open Source Paradigm Shifts (2004), where he discusses the PC value chain, IBM commoditized the hardware and value migrated up to Microsoft’s operating system—but it also migrated down to Intel’s microprocessor. Neither direction was obvious in advance. The winners were the ones who understood the new architecture before everyone else did.

The same uncertainty applies here. If stablecoins become the commodity instrument of public-facing payments, value may migrate up to the platforms and AI agents that programme money most effectively. Or it may migrate down, to whoever controls the settlement infrastructure that everything else depends on. We do not know yet. What we do know is that every layer is a candidate—and that any power that cedes a layer has already conceded the argument about where value ends up.

In other words, every sovereign currency that wants to remain relevant in the tokenized economy needs representation across all four levels. Miss a floor and the whole structure waits for a crisis to expose the gap.