Wide Open, Locked In

China is open-sourcing its intelligence, America is open-sourcing its currency, and the two are building a new version of the same old trap

For decades, America and China have been locked in a structural embrace that neither could easily escape. China manufactured; America consumed. China saved; America borrowed. The dollars that Americans spent on Chinese goods flowed back across the Pacific as purchases of US Treasury bonds, financing the very deficits that kept American consumers buying. Economist Michael Pettis calls this “vendor financing”. Others call it a trap.

The trap worked because the two economies were mirror images. China suppressed domestic consumption—through low wages, restricted social safety nets, and financial repression—to make its manufacturing hyper-competitive. Meanwhile, America ran persistent trade deficits because foreign capital needed somewhere safe to go, and the dollar was the only candidate. Each country’s model required the other’s. Neither could change course without threatening the foundations of its own system.

Fast forward to today’s new technologies and paradigm shift: AI. When looking at the current AI race, most often observers tend to frame it as a clean break: a new technological order that reshapes global power. But the deeper pattern is replicating itself— with one crucial difference: this time, each side is choosing its exposure. China is open-sourcing its intelligence, America is open-sourcing its currency, and the two are converging in the emerging economy of AI agents—each opening its strength, each exposing its flank.

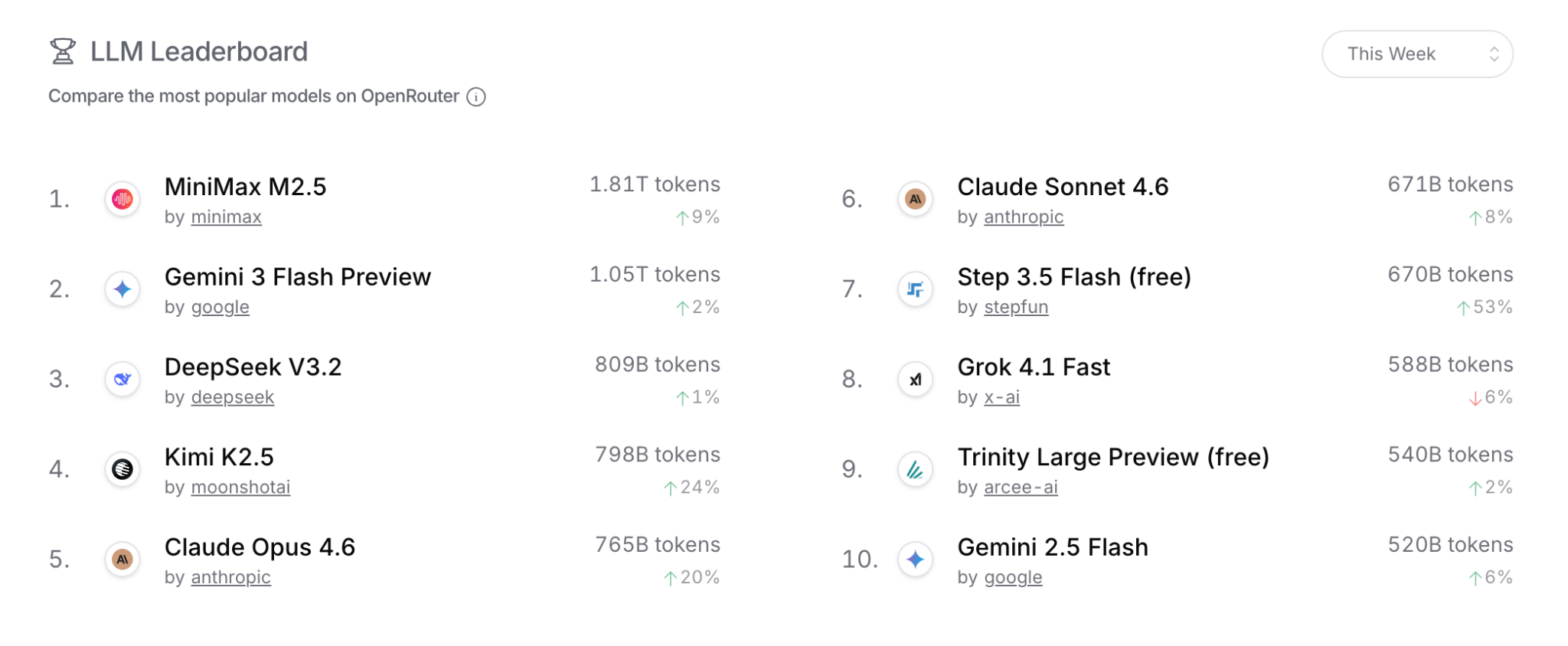

What OpenRouter Tells Us

Let’s look at OpenRouter’s traffic data. Three of the six most-used large language models in the world, by actual production volume, now come from Chinese laboratories. MiniMax M2.5 sits at the top. DeepSeek and Zhipu’s GLM follow closely behind. The largest single consumer of AI inference on the open market is OpenClaw, an autonomous coding agent that routes the bulk of its traffic through Chinese models.

Open Router Data, March 8th, 2026

The mechanism is straightforward price arbitrage. MiniMax M2.5 matches Claude Opus 4.6 on software engineering benchmarks—80.2% versus 80.8%—and costs roughly one-seventeenth the price per token. A workload that costs $100 a day on Claude costs under $5 on MiniMax. Agents, which are indifferent to national origin and acutely sensitive to cost, make the obvious choice.

The economics are not purely a software achievement. China’s total installed power generation capacity reached 3,349 GW by end of 2024. Wind and solar alone hit 1,406 GW, surpassing China’s own 2030 target six years early. Clean energy now accounts for 52% of installed capacity. China spent $625 billion on clean energy in 2024—31% of the entire global total. Compute requires electricity. Cheap, abundant electricity makes cheap inference possible. The price gap between Chinese and American AI is partly an energy infrastructure story, built over decades of directed investment. The US, by contrast, faces genuine data centre power constraints. New capacity is queued behind grid limitations that will take years to resolve.

Then there is the architecture. DeepSeek’s Mixture-of-Experts design activates only a fraction of its parameters during inference. MiniMax M2.5 runs 229 billion total parameters but activates only 10 billion per query. These are structural cost advantages that compound at scale.

Finally, layered on top is straightforward competitive pressure: a dozen Chinese AI companies—Alibaba, ByteDance, Baidu, Tencent, Moonshot, Zhipu, MiniMax and others—compete so aggressively on price that margins have long since turned negative. They are buying market share, and it is working. The consequence extends beyond price. Every query routed to a Chinese model is also a transfer of data onto infrastructure subject to Chinese law. The cost advantage and the data advantage are the same advantage—and the data vulnerability for everyone else is the same vulnerability.